The Best Travel Credit Cards for Families (Our Beginner-Friendly Picks)

How We Got Started With Points and Miles

Learning to use points and miles has completely changed the way our family travels. It has made travel more accessible for our family of four and allowed us to take trips that honestly wouldn't have been possible otherwise.

And let me tell you…we didn't learn this overnight. We made plenty of mistakes along the way, AND we're still learning. We just want to share what's worked for our family in hopes that it helps yours travel a little more, too.

We always valued family vacations, but we wanted to see more of the world together. After experiencing some serious sticker shock while planning a trip overseas to visit family, we realized that if we wanted to keep traveling, we needed to find a smarter way to pay for it.

We weren't looking for luxury travel (well...not at first anyway!). We weren't trying to fly first class around the world or stay in five-star hotels (although we definitely wouldn't have turned it down!). We simply wanted to be able to say "yes" to more family adventures without blowing our budget.

And that's where points and miles came in.

Before learning about travel credit cards, we already earned the occasional hotel point here and there from work trips or hotel stays. Those points were nice, but a discounted hotel room or a free night at a Fairfield Inn isn't exactly what gets a family of four to England.

Suddenly, the trips we'd been dreaming about (and the one we didn’t even dare to dream about) actually felt possible.

Since then, we've used points and miles to help our family travel to places like the Bahamas, Puerto Rico and Europe, and we're currently planning an almost entirely points-funded trip to Italy.

And I don't just mean opening one travel card and putting all of your purchases on it (although that's a huge step up from where we started!). I mean strategically opening more than one travel credit card over time to earn welcome offers and build points much more quickly.

Before we go any further...

We only recommend using travel credit cards if you pay your balance in full every month. The value of points and miles is quickly outweighed by interest charges, so this hobby isn't worth it if you're carrying credit card debt.

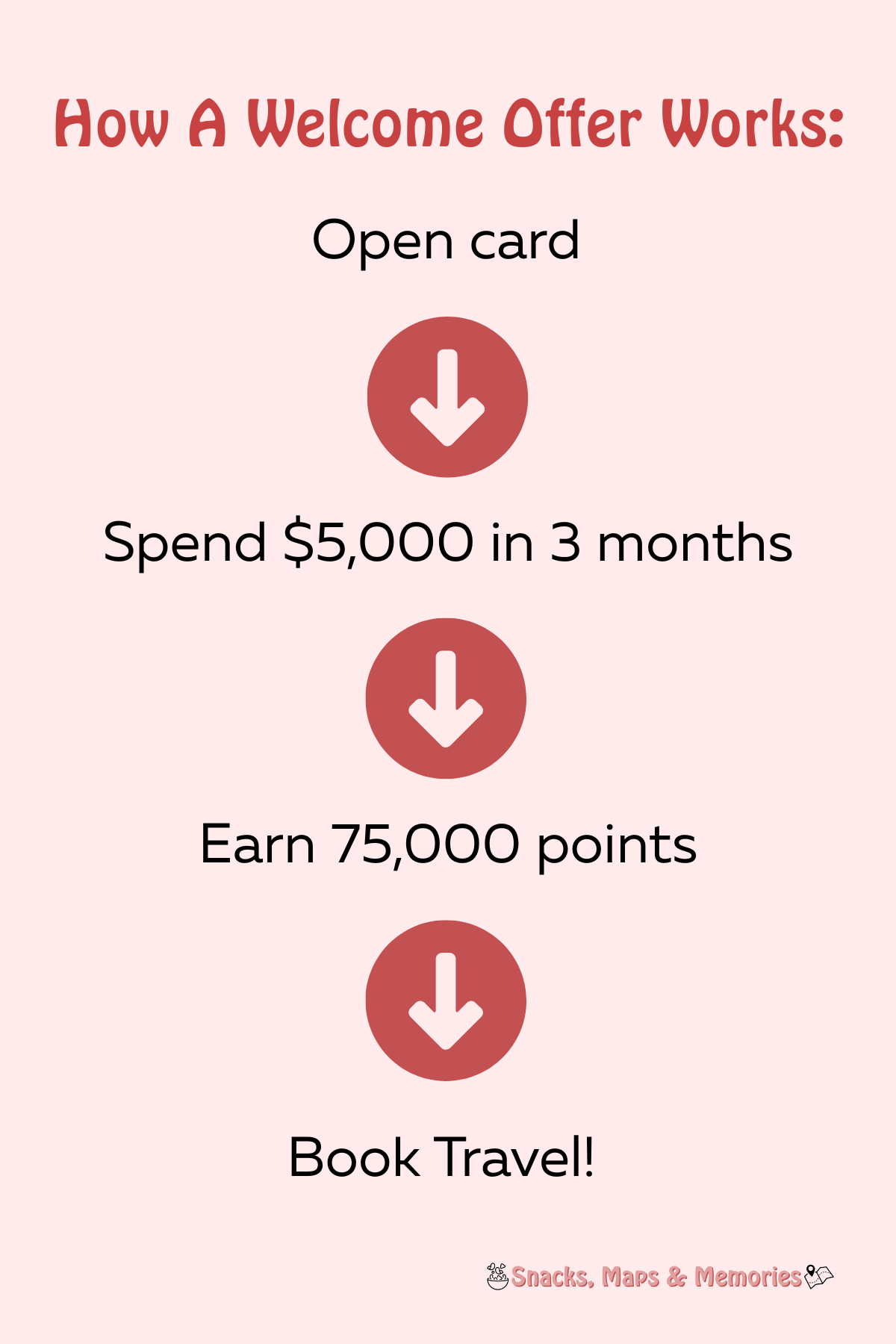

What Is a Welcome Offer?

A welcome offer is a large number of points or miles that you earn after opening a new travel credit card and spending a certain amount within a specific timeframe.

For example, one of the cards we recommend most often, the Chase Sapphire Preferred®, typically offers 75,000 bonus points after spending $5,000 in the first three months. Occasionally, Chase even offers an elevated welcome offer with even more points.

That's a significant amount of points that can go a long way toward paying for a family vacation.

How We Earn Welcome Offers

One of the questions we get asked most is, "How do you earn so many points?"

Our answer is actually pretty simple.

When one of us opens a new card, we both add that card to our Apple Wallet and make it our default payment method. We put as many of our normal monthly expenses as possible on that card until we've reached the minimum spending requirement.

In other words, we work on the minimum spend together.

Once we've earned the welcome offer, the other person opens the next card, we switch our default payment method, and repeat the process.

Rinse and repeat.

One important note: We only recommend this strategy if you're able to pay your credit card balances in full every month. Travel rewards are never worth paying interest for.

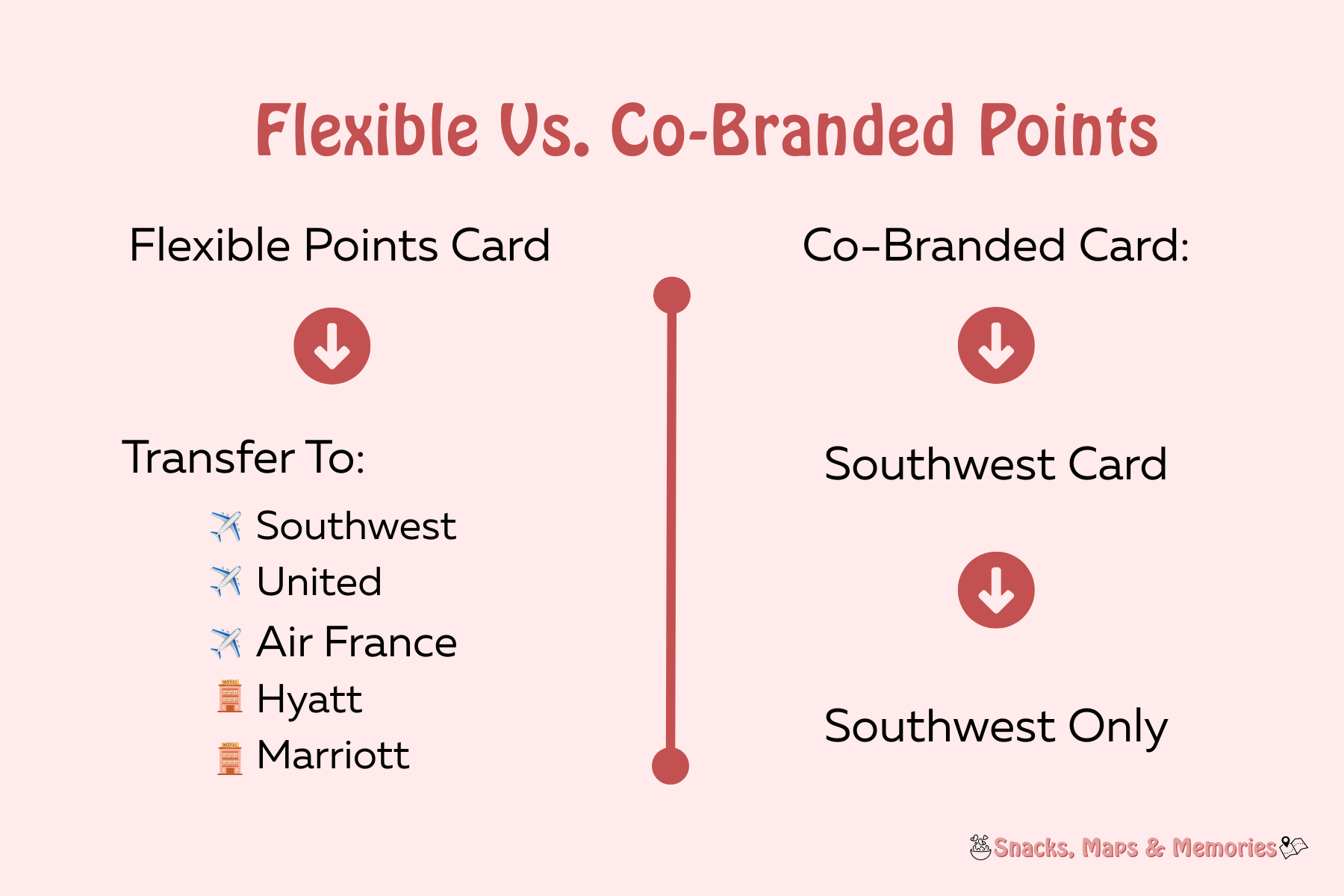

Why We Recommend Flexible Points

If you're just getting started with points and miles, we almost always recommend beginning with flexible points instead of airline- or hotel-specific cards.

The three cards we're about to recommend all earn flexible points, which means those points can be transferred to multiple airline and hotel partners instead of being tied to just one brand.

For example, a Southwest credit card earns Southwest points. A Hyatt card earns Hyatt points.

Those can be fantastic cards if you already know you'll use those brands regularly.

But for most beginners, flexible points give you far more options.

Maybe one airline has a great deal to Europe, while another has the best flights to the Caribbean. Maybe Hyatt has availability for one trip, but Marriott works better for the next. Flexible points let you choose what works best instead of forcing your vacation to fit your points.

That flexibility has been incredibly valuable for our family.

Now, if you're someone who spends a lot of weekends at Marriott hotels for your kids' travel sports tournaments and you'd like to use points to cover those stays (or extend those weekends into mini family vacations!) a co-branded card might actually be the perfect place for you to start.

That's why flexible points are where we recommend almost every beginner starts. As you become more comfortable with points and miles, you can always add co-branded cards later if they make sense for the way your family travels.

Why We Chose These Cards:

We didn't choose these cards because they're flashy or because they have the biggest welcome offers. We chose them because they check the boxes that matter most to our family. In fact, two of these are the very cards we started with.

Great welcome offers

Flexible points

Reasonable annual fees

Valuable travel protections

Transfer partners we actually use

Easy to keep long term

There are dozens of travel credit cards out there, but if we were helping a friend get started tomorrow, these are the three we'd recommend first.

So...without further ado, here are the three travel credit cards we'd recommend to almost anyone getting started with points and miles.

Our Top Three Travel Credit Cards For Beginners:

Card #1: Chase Sapphire Preferred®

Current points earning:

5x points on travel purchased through Chase Travel℠

3x points on dining

3x points on select streaming services

3x points on online grocery purchases (excluding Target, Walmart and wholesale clubs)

2x points on all other travel purchases

1x point on everything else

This is a cool little card. For a low annual fee, this card usually has a nice welcome offer, and it offers a $100 travel credit that you can use in the Chase travel portal. That $100 credit covers the annual fee alone.

This card also offers up to a $120 credit towards TSA precheck, Global Entry or NEXUS every four years, and a complimentary Dashpass membership with $10/month off of groceries, daily essentials and more through Dashpass delivery.

Chase has some less common transfer partners such as Southwest airlines, United airlines and Hyatt, making it a desirable card to have your wallet if you want to travel using any of those brands.

One of our favorite features, and one that often gets overlooked, is the travel insurance. This card includes trip delay, trip cancellation/interruption, lost baggage protection and primary rental car insurance. That's impressive for a card with such a modest annual fee.

We used to purchase travel insurance separately for almost every big trip because, well...kids. Flights get delayed, people get sick, luggage gets lost. Since getting the Chase Sapphire Preferred, we simply make sure to pay for at least part of our trip with this card so those protections kick in. We've actually had to use them before, and having that peace of mind has been worth it.

If you use one of our links to apply for this card, we get referral points from Chase’s Refer A Friend program (different than an affiliate link).

Card #2: Capital One Venture

This card is so easy.

You earn 2 miles on every purchase, regardless of category, and 5 miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel.

The welcome offer is typically around 75,000 miles after spending $4,000 in the first three months.

No muss, no fuss.

We tend to think of our Capital One miles as our "international flight miles" because of the airline transfer partners we typically use, but you certainly don't have to think about them that way.

One feature we really love is the ability to erase eligible travel purchases within 90 days. That means if you book something that isn't easy to pay for with points…like Disney tickets, campground reservations or many vacation rentals, you can often redeem your miles afterward as a statement credit. It's one of the most flexible ways to use travel rewards.

If you use our referral link to apply for a Capital One Venture Card then we earn points for referring - thank you!

Card #3: Citi Strata Premier

Points earning

10x points on hotels, car rentals and attractions booked through Citi Travel

3x points at restaurants

3x points at supermarkets

3x points at gas stations

3x points on air travel and hotels

1x point on everything else

We think this card is one of the most underrated travel cards available.

Like the other cards on this list, it typically comes with a generous welcome offer and a reasonable annual fee. But what really makes it stand out is its transfer partners.

Citi recently added the ability to transfer ThankYou Points to American Airlines AAdvantage®, making this card especially valuable for families who live near an American Airlines hub or frequently fly American. Since we live in North Carolina, American is one of our primary airlines, so this addition made the Citi Strata Premier much more attractive for our family.

The bonus categories are also practical for everyday spending. Earning 3x points on groceries, restaurants and gas means you can continue building points long after you've earned the welcome offer.

Which card should you get first?

If you're brand new to points and miles, our recommendation is simple.

Start with the Chase Sapphire Preferred.

It has an excellent welcome offer, fantastic travel protections, valuable transfer partners and an annual fee that's easy to justify.

Once you've earned that welcome offer, consider adding the Capital One Venture Rewards or Citi Strata Premier to diversify your points and give yourself even more travel options.

Remember, you don't need ten credit cards to travel well. We certainly didn't start there.

We simply opened one card, earned the welcome offer, then opened the next card once we finished the minimum spending requirement.

Little by little, those points added up.

Today they've helped our family visit places we never thought we'd be able to afford…from the Bahamas to Europe…and they've completely changed how we think about paying for travel.

If you're just getting started, don't overcomplicate it.

Pick one good card, learn how it works and build from there.

Frequently Asked Questions:

If you open multiple cards, do you keep them open forever?

No. In fact, many people don't.

There are two best practices we like to keep in mind.

First, keep the card open for at least 12 months. Opening a card, earning the welcome offer, and immediately closing it doesn't build a great relationship with the bank. With many cards, if you wait until the annual fee posts after your first year, you can cancel or downgrade the card within about 30 days and have that annual fee refunded.

Second, consider keeping your oldest card with each bank. Having a longer history with a bank can be beneficial, and many cards can be downgraded to a no-annual-fee version if you decide the benefits no longer justify paying the annual fee.

How do you keep track of the cards you open?

We use the Travel Freely app, and it's one of our favorite tools for staying organized.

It keeps track of when we opened each card, when we earned the welcome offer, and how many points we've earned throughout the year. It also sends reminders when a minimum spending deadline is approaching or when an annual fee is about to post so we have time to decide whether we want to keep, downgrade, or cancel the card.

For us, it's much easier than trying to keep track of everything in our heads or even on a spreadsheet.

What kind of expenses do you put on your card to meet the minimum spend?

For most welcome offers, we simply use our normal monthly expenses.

That includes things like:

Groceries

Dining out

Shopping

Kids' activities

Travel expenses

Gas

Utilities

Insurance premiums when possible

We're not spending extra money just to earn points. We're simply putting purchases we were already planning to make on the new card.

If we're working on a larger minimum spending requirement…or just want to finish it more quickly. We may also pay estimated taxes with a credit card, even though there's typically a small processing fee.

We also get asked about store credit cards like the Amazon Prime Visa or Target Circle Card. Unless we're working on a particularly large minimum spend, we usually continue using those cards at Amazon and Target because the 5% savings is tough to beat. But if we needed a little extra spending to earn a welcome offer, we'd happily switch those purchases to the travel card for a while.

Do I have to spend extra money to earn the welcome offer?

No, and we actually don't recommend thinking about it that way.

Our goal is to take money we're already planning to spend and make it work harder for us. Instead of earning very little on our everyday purchases, we'd rather earn points that help pay for future travel.

If earning a welcome offer requires you to spend money you wouldn't have spent otherwise, it's probably not the right card…or the right time…to open it.

Will opening a new credit card hurt my credit score?

It might cause a small, temporary dip, and that's completely normal.

If you continue paying your credit card balances on time and in full, many people see their credit score recover fairly quickly. Over time, responsible credit card use can even improve your credit score.

Of course, everyone's credit profile is different, so your experience may vary.

How many travel credit cards should I open each year?

A common guideline in the points and miles world is to open one new card every 90 days per person.

For a two-person household, that could mean each person opens four cards per year, for a total of eight welcome offers.

That said, we don't follow that rule perfectly.

Sometimes we'll open a card a little sooner if there's an especially good welcome offer available. Other times we'll wait longer because we don't have a specific trip in mind.

We tend to alternate between Jeff and me, giving ourselves plenty of time to meet the minimum spending requirement before opening another card.

Can both spouses (or partners) earn the same welcome offer?

Yes!

In fact, many of our favorite cards are cards that both Jeff and I have opened.

Since welcome offers are earned by the individual cardholder, each person can often earn the same bonus on their own account, provided they meet the card's eligibility requirements.

What is a transfer partner?

Think of transfer partners as airlines and hotels that let you move your flexible points into their loyalty program. When you opt into a free rewards program, like Southwest or Marriott, where you earn points by flying or staying with them, you can now transfer the points you earn on your credit card into your free rewards account and wah-lah! Now you have Southwest or Marriott points to use towards free flights or nights stay.

This usually results in a better value than booking the same flight or stay through your credit card travel portal and you can earn points faster on your everyday spend with your credit card.

You can't reverse a transfer, so we only transfer points after we've found the flight or hotel we want to book.

Do I need to travel a lot to make travel credit cards worth it?

Not at all.

One of the biggest misconceptions about travel credit cards is that they're only for people who travel all the time.

We actually think they're incredibly valuable for families who take just one or two trips each year.

Whether you're using points to cover hotel stays for your kids' sports tournaments, visit family, take an annual beach vacation, or finally book that bucket-list trip you've been dreaming about, travel rewards can help make those trips more affordable.

That's exactly why we got into this hobby in the first place!